A guide to increasing take up of the savings option on the Standard Financial Statement (SFS) or its equivalent form.

Having savings helps to prevent financial difficulties. The Money and Pensions Service (MaPS) has developed behavioural science ‘nudges’ to encourage debt advice clients to save or continue saving during their debt plan. These nudges can be used by advisers when establishing or reviewing debt solutions. While not everyone’s financial circumstances will allow them to save, many others will have this opportunity through the (SFS) savings category.[1] MaPS is keen to promote this option.

The guide is the result of collaborative efforts between MaPS and two different debt advice providers that put the initiative into practice: Angel Advance, a fee-charging debt management company; and Christians Against Poverty (CAP), a charitable organisation giving free debt advice.

MaPS encourage debt advice service providers to introduce the learnings in this report. Doing so will help avoid repayment plans being disrupted and reduce the risk of clients falling into problem debt, so even more people can be supported by the sector.

The impact

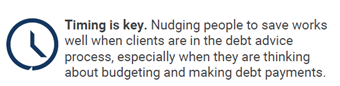

To measure its effectiveness, the study run over a five-month period and compared change between a treatment group of clients who experienced the nudges and a control group of clients who did not.[2]

Framing savings as a way to create financial resilience and using mental accounting had the greatest impact among the different nudges used.

Creating a ‘safety net’ of savings to be resilient against financial shocks, such as unexpected bills, has the largest impact when motivating clients to save with 43% of clients in the treatment group were definitely encouraged to save or continue saving compared to 32% in the control group.

[1] The regular savings option on the SFS or equivalent form allows debt advice clients to keep a small amount of unassigned savings for future use (up to 10% of available income, with a cap of £20 per month, for the SFS). These statements are used by advisers to summarise a client’s income and outgoings, along with details of any debts. All clients agreeing a debt solution complete an SFS or comparable statement, which is reviewed, often yearly.

[2] For evaluation purposes, this initiative focused on one debt solution: the Debt Management Plan (DMP), a formal agreement between a debtor and a creditor, allowing the debtor to pay off non-priority debts at an affordable rate. It can also be used with other debt solutions.

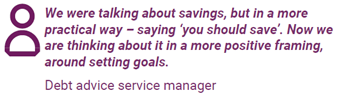

Framing saving with a specific goal to achieve in a specific time has a significant positive effect in the numbers of clients choosing the savings option on their Standard Financial Statement (SFS) or its equivalent. 44% of clients in the treatment group found this very useful for them to save or continue saving compared to 33% in the control group.

Results also show a clear link between positive financial behaviours and clients who have less time remaining on their repayment term, as well as positive financial feelings and behaviours for longer term clients (with a relationship of six months or over).

Nudges can be used in combination with an automatic saving opt-in when agreeing a debt solution.

By encouraging clients to save in an empathetic way, we can overcome the financial circumstances and psychological barriers that prevent indebted individuals from putting money away. Promoting a regular savings habit has the potential to change lives and free up advisers’ time to help even more people.

Download the guide

The guide is available to download here. This includes practical recommendations to streamline this initiative and guidance for conversational nudges, online and paper communication alongside the behavioural nudges used.

Innovate with us! For more information about this resource or to get involved in our innovation projects, please contact MaPS innovation team at Innovatingtogether@maps.org.uk